Bitcoin, Strategy, and the Delicate Recursive Wealth Machine Michael Saylor Built

Why It Works, and Why It Is Breaking!

Lunch with Michael Saylor … It explained everything about his Bitcoin empire.

By David Buzzelli

Founder | Builder | Observer of Recursive Systems

Not long ago, I enjoyed lunch at Michael Saylor’s estate in Miami Beach.

We were met beyond the gates by a security team who received us onto the property. I had brought something unusual — a quadruped robot, one of my own research projects. After some discussion with the guards, we booted it up and had it walk toward the outdoor dining area, where a long table was set — easily enough for 20 guests, surrounded by other tables and shaded courtyards. Behind us, a superyacht appearing to be over 100 feet long sat docked — presumably his, as it was moored directly behind the estate on the Intercoastal.

I had also brought along Jeremy Rubin, one of the early technical pioneers in Bitcoin development. They had never met. Jeremy’s work helped push the boundaries of programmable money years before it was mainstream. Saylor hadn’t expected him.

We talked about robotics, Bitcoin, and Ethereum. I made a point — intentionally — that I believed Ethereum served a valid and distinct role in digital capital formation, separate from Bitcoin. I still do. It was clear that this wasn’t a welcome perspective.

Saylor smiled, but a group of young model-type women seated nearby at the table — part of his curated guest list — laughed in a way that made it clear: this wasn’t just disagreement. This was dismissal.

Moments later, we were asked to relocate — to another table inside a separate guest house. Saylor stayed at the main table with his guests. Jeremy, myself, a few others, and the robot dog ate lunch alone.

It wasn’t offensive — just instructive.

That moment became a working metaphor for what I have come to see Saylor’s market positioning as:

A controlled stage. A dominant narrative. And a firm boundary between those who reflect the message and those who disrupt it.

That day wasn’t about the food or the technology. It was a live demonstration of the philosophy behind his corporate and market approach: control the frame, steer the narrative, and insulate the signal from disruption. In my opinion, what he mirrors in business was the financial equivalent of that lunch — a carefully architected structure where belief, repetition, and access define value more than fundamentals. To understand what Saylor built with Strategy, you have to look beyond Bitcoin and into the recursive financially engineered loop itself.

The Game - Is this “A house of cards” That Strategy (Formerly MicroStrategy) Built?

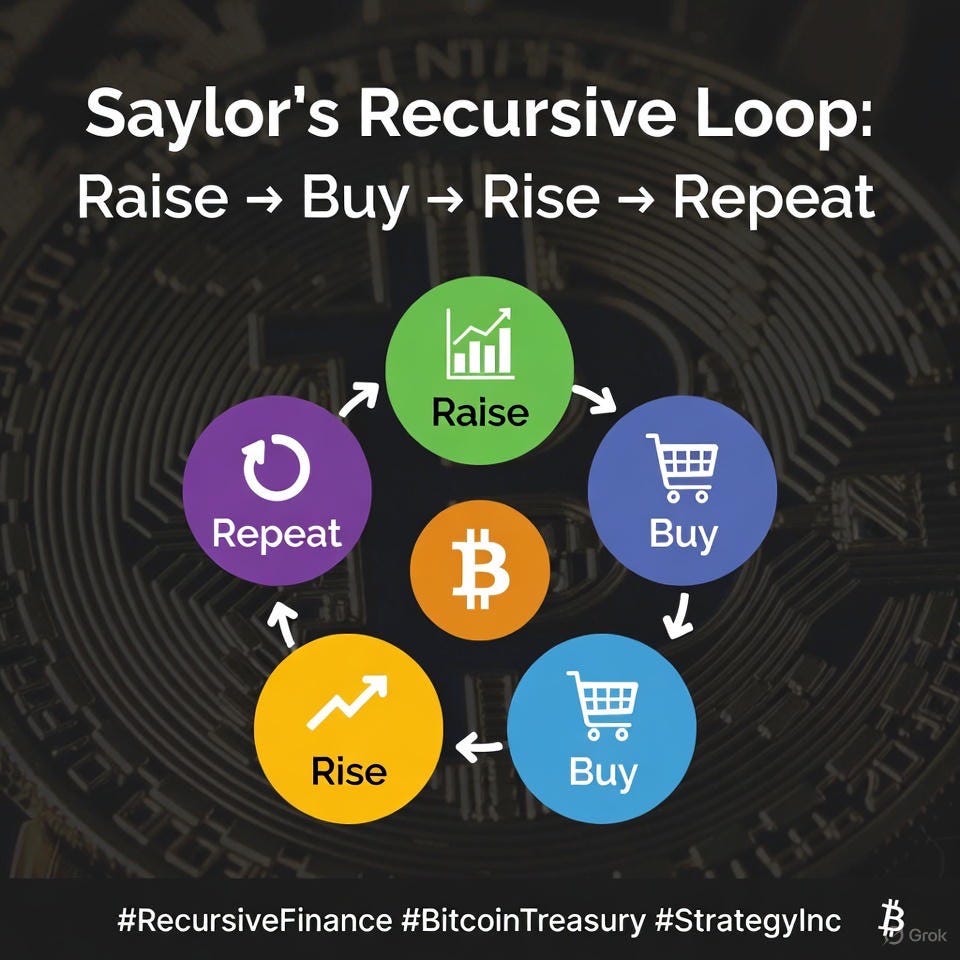

In the last few years, Michael Saylor has turned a sleepy enterprise software company into a high-octane Bitcoin-backed capital engine. He did it not by building new software or discovering new revenue — but by mastering a recursive loop:

Raise capital → buy BTC → increase equity value → raise more capital → repeat.

It’s elegant. It’s aggressive. And, until recently, it worked.

Saylor’s “Strategy” (formerly MicroStrategy) created one of the most inventive capital flywheels in public market history — a loop powered by Bitcoin scarcity, belief, and legal leverage.

But now, as the stock trades below the value of its Bitcoin holdings for the first time, and as he layers on convertible bonds, preferred shares, and synthetic derivatives — many of us are asking:

Is this still financial strategy — or has it become something else entirely?

Recursive Value Creation: The Legal Financial Perpetual Motion Machine

At its core, Saylor’s strategy is simple recursion:

1. BTC is the collateral layer

2. Stock price rises on narrative

3. Equity + convertibles = leverage

4. Leverage buys more BTC

5. Go back to step 1

Each of these steps is legal. None of them, individually, trigger alarms. But the structure as a whole creates a synthetic exposure spiral — not unlike rehypothecation in the old shadow banking system.

The company issues:

• Convertible bonds (e.g., March 2030 notes with embedded call options at 0% interest, ~$8B outstanding + $14B pipeline)

• Perpetual preferred shares (STRK: 8% convertible hybrid, $22B ATM; STRF: 10% senior fixed, $3B; STRD: 10% junior non-cumulative; STRC: variable-rate for yield chasers)

• ATM equity raises (e.g., $21B MSTR common + $21B STRK programs at premium valuations)

• No operational profit required—just belief and Bitcoin

This layers synthetic claims on the BTC base, creating ~2.8× effective leverage to Bitcoin exposure via converts + preferreds: the same ~$61B in holdings now backstops multiple rounds of debt, equity, and hybrids—rehypothecating one BTC up to three times across the stack.

The result? A circular stack of financial claims built on the same core asset.

Saylor’s Counter: The Moat of Belief

To be fair, Saylor would counter—and has—that the premium itself is the moat. He frames Strategy not as a software company with a Bitcoin side hustle, but as the network steward of digital capital belief.

In his view, the stock’s historical 2–4× NAV premium isn’t speculation; it’s network effects in action—a self-reinforcing loop where institutional adoption, media amplification, ETF inflows, and corporate treasury mimicry compound the narrative. “Bitcoin is the apex property,” he says, “and Strategy is the public-market on-ramp.” The higher the premium, the cheaper the capital, the more BTC acquired, the stronger the signal. It’s not a bug; it’s the business model.

But here’s the fracture: network effects decay when the belief is no longer scarce. Once every public company, pension fund, and sovereign balance sheet can copy the playbook—once Bitcoin ETFs hold 5% of supply and corporate treasuries mirror the loop—the uniqueness evaporates. The premium was never backed by software margins or patents; it was backed by asymmetric conviction. When that conviction becomes consensus, the moat fills with water.

Today’s -2.3% discount isn’t volatility—it’s the market pricing in the death of exclusivity. The loop still spins, but the flywheel is now shared, not owned.

The Premium Collapses — A Market Concern

In late 2025, that belief cracked.

For the first time, Strategy’s market cap dropped below the value of its Bitcoin holdings.

As of market close on November 14, 2025 (4:00 PM ET), MicroStrategy’s market capitalization traded at an approximate -2.3% discount to the net asset value (NAV) of its Bitcoin holdings. This marks the continuation of the recent unwinding of the stock’s historical premium, with the discount deepening slightly from intraday lows but remaining narrow.

This is more than a technical data point — it’s the unwinding of a recursive narrative premium. The market stopped believing the equity should trade above NAV.

Why?

Rising BTC volatility

Overcomplicated capital stack

Regulatory scrutiny of treasury disclosures

Diminishing marginal returns on each additional BTC buy

No real business underneath — just leverage and exposure

This is the moment the recursive loop hits the edge of its own logic.

The Grey Area: Why Is This Legal?

Skeptics are right to ask:

How is this allowed? Why can a public company build a circular valuation machine?

The answer lies in the structure of the law.

Each piece of the strategy is legal on its own:

Holding Bitcoin? ✅ Legal

Issuing debt to buy assets? ✅ Legal

Raising equity? ✅ Legal

Letting investors price your stock irrationally? ✅ Still legal

Regulators don’t police financial recursion, yet — they police disclosure, fraud, and systemic harm. Unless Strategy misleads investors or triggers contagion, it’s just… capitalism.

But don’t mistake legality for integrity. This is a legal infinite loop, not a sustainable operating model.

The Myth of Digital Capital = Bitcoin

Perhaps the biggest distortion isn’t in the financing — it’s in the narrative.

Saylor has claimed:

“Bitcoin is the apex digital property.”

“There is no second best.”

“Bitcoin is the one true digital capital.”

“Own 1/21,000,000 of all Digital Money”

This is false. Single killer stat: “ETH alone has settled $11T in 2024 vs BTC’s $2.3T—programmability is capital formation.”

Bitcoin is a scarce, non-sovereign store of value. It may be the purest form of digital belief capital — but it is not all digital capital.

There are:

Programmable assets (ETH, SOL, L2s)

Yield-bearing protocols (DeFi lending, staking)

Real-world tokenized assets (RWAs)

Governance-based DAOs

Synthetic assets and wrapped derivatives

To collapse all of that into Bitcoin is a rhetorical sleight of hand. It ignores utility, composability, productivity, and capital diversity.

In truth, Bitcoin is layer one belief, not layer zero reality.

What This Means for Analysts, Regulators, Investors, and Small-Caps

As part of a broader research exercise, I explored whether smaller public companies could replicate the Strategy playbook — pooling resources to buy BTC, raising debt on treasury exposure, and benefiting from the recursive valuation loop.

The answer: yes, technically. But beware:

It works until it doesn’t.

When the narrative premium collapses, the loop turns in on itself.

The capital stack becomes fragile, not antifragile.

Disclosure risks rise, especially if the equity premium is the primary value driver.

In a world where market caps move faster than operating profits, recursive capital strategies are seductive. But they are not immune to gravity.

What Comes Next: Decentralized Treasury Strategy?

If we’re honest, Saylor’s loop is just the beginning. What he built is a crude prototype for:

Future on-chain corporate treasuries

DAO-governed financial loops

Multi-asset, multi-layer treasury allocations

Tokenized balance sheets where equity and crypto assets blur

In the next phase, the recursive loop won’t be hidden in equity and convertibles. It will be visible, composable, and programmable.

That’s where the real game begins.

Final Thought

The problem isn’t Bitcoin.

The problem isn’t leverage.

The problem isn’t Michael Saylor.

The problem is pretending recursion is value creation.

Michael Saylor envisioned the loop before most people did. He built it, scaled it, and — for a time — it worked.

That lunch told me everything: control the guests, dismiss dissent, move the noise elsewhere. The same playbook runs under Strategy’s financial engine — a recursive machine powered not by Bitcoin, but by narrative discipline.

If you’re building the next one — don’t copy the myth. Copy the mechanics and build with transparency.

“All financial data sourced from public sources, SEC filings, Bitcoin dashboards, and market close 11/14/25. Opinions are the author’s.”

#Bitcoin #MichaelSaylor #StrategyInc #RecursiveFinance #BitcoinTreasury #OnChainTreasury #NAVdiscount #DigitalAssets #CorporateBTC #Saylorium #HouseOfCards? #MSTR #Crypto

$50K is a “convex test” — downside capped at ~48% BTC loss, but Saylor’s flywheel (cheap debt + HODL conviction) keeps it afloat. It’s asymmetric: Survive the winter, thrive in spring. (Peter Brandt sees $50K as possible bottom; Saylor’s already tweeting “We’re ₿uying.”)

Time Horizon Mismatch Creates Edge … his strategy is based on decades. He out-waits panic sellers and short-term noise.